Based on recent Canada Census statistics, we can estimate that nearly 1 of every 5 Canadians are over the age of 65. Retirement at 65 or younger is still the Canadian dream, and while more people are working longer to supplement their retirement income, others rely on passive income from their investments, primarily dividends, to enjoy a comfortable retirement.

GIC’s just don’t cut it. Three-year rates are less than 2%. Investors seeking better returns are turning to the stock market where dividend yields are more attractive. “Blue-chip” companies like the banks are paying 3% and 4% or more per year with the potential of capital appreciation to boot. The most important consideration for retirees who need this supplemental income is reliability.

Dividend payers must deliver every quarter or every month to provide needed income. On top of that, retirees can’t afford a major collapse in their account size in their twilight years, so consistent and predictable share prices are important too. Modest capital appreciation is a bonus, but capital preservation is most important at this stage of life.

The question for many retired or soon-to-be-retired investors is, “Can you get decent returns with the comfort of knowing you own shares of companies that are well-positioned to keep the dividends coming while maintaining and possibly growing their share price in the short to medium term?” The answer is “Yes” if you have the research and analysis tools such as we have in VectorVest.

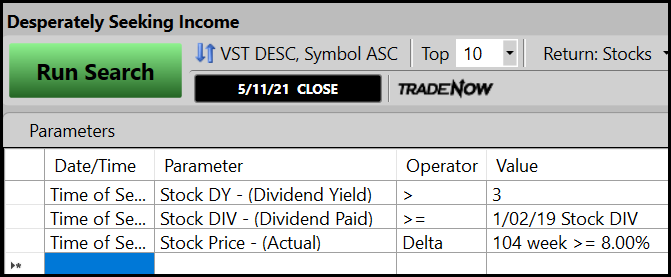

Here is a simple little search I created to narrow the stock selection based on the first two objectives—a decent and reliable income. My first parameter is DY (Dividend Yield) greater than 3%. The second parameter is DIV (Dividend Paid) greater than or equal to the Dividend paid on January 2, 2020. The results are surprising. More than 250 stocks met that basic criteria as of Tuesday, May 4th. Imagine, well-known, solid companies like Great-West Life, GWO, paying a DY of 4.87% per year. Rogers Sugar, RSI, headquartered just down the road from me in Taber, Alberta, 6.46%; Capital Power, CPX, 5.13%; Power Corp, POW, 4.91%; Superior Plus, SPB, 4.71%, Canadian Imperial Bank, CM, 4.54%, and BCE Inc, BCE, 5.98%.

Click or tap image to enlarge.

Next, I added just one more parameter. Stock Price (Actual), Delta 104 week >= 8.00% as I wanted to see a modest 8% capital appreciation, or 4% per year over the previous two years (104 weeks). Now I have 118 stocks to choose from that meet the criteria. BCE and RSI were eliminated from the above list because they did not meet the 8% capital appreciation over two years. Other notables that met the criteria include Sun Life Financial, SLF, 3.31%; TD Bank, TD, 3.75%; National Bank, NA, 3.17%; IGM Financial, IGM, 5.03%; Bird Construction, BDT, 4.22%; CT REIT, CRT.U, 4.81%; Granite Real Estate, GRT.U, 3.74%; and two of my favourite utilities, Emera Inc, EMA, 4.54% and Fortis Inc, FTS, 3.69%.

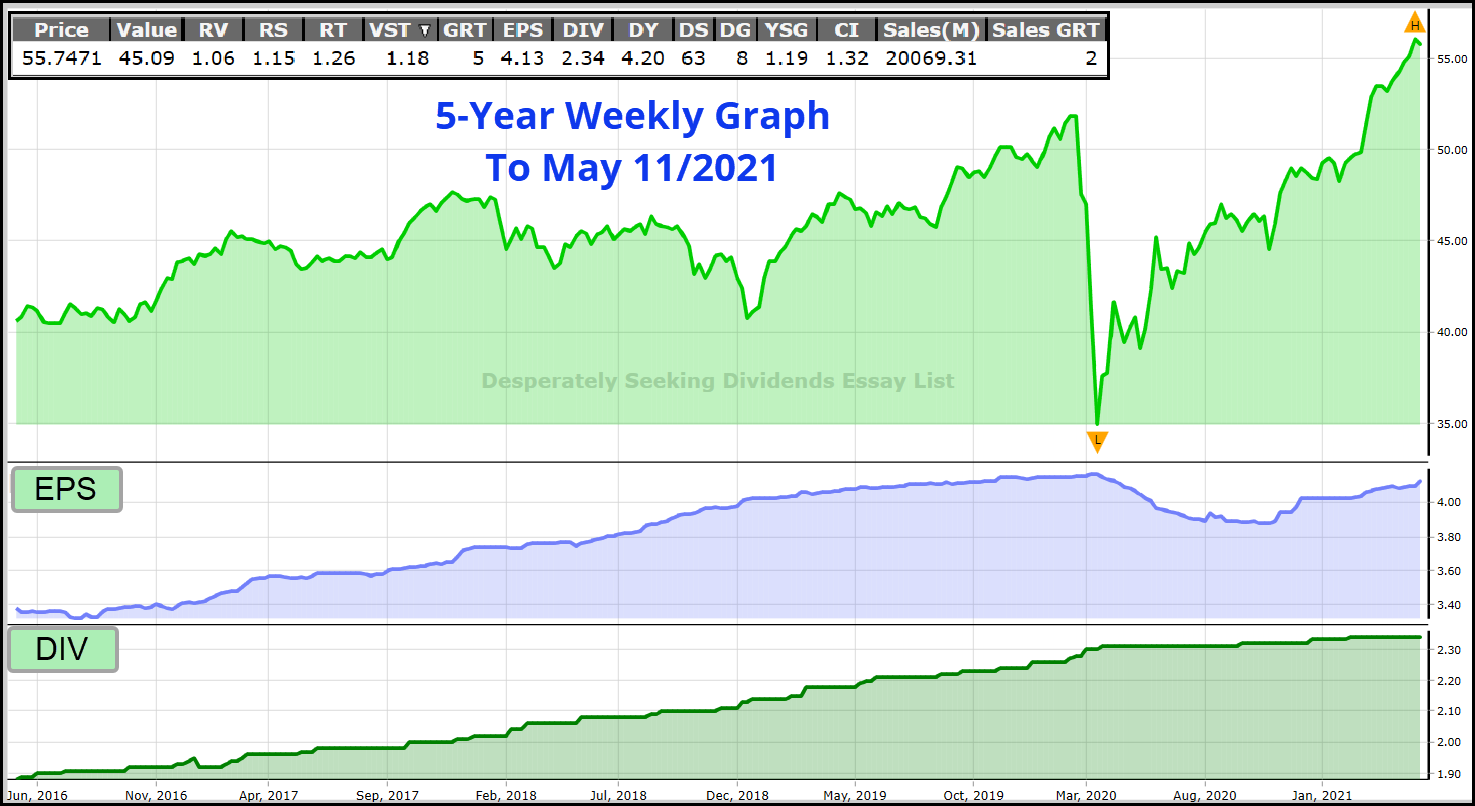

The graph below is a WatchList Average Graph displaying the average price, EPS and Dividend Payments of all the above-listed stocks.

Click or tap image to enlarge.

Once you have these stocks in a WatchList, the next step is to study at least a two-year graph with Price, Earnings Per Share, and Dividends paid. I am looking for consistency with all three. Finally, favour those stocks with the highest Relative Safety and Dividend Safety scores, and wait for them to get VectorVest’s Buy rating before stepping in. You will have done the best you can do, as much or more than almost any paid advisor could do for you.

To learn more, please join me for our regular Tuesday, CA Special Presentation Q&A at 12:30 pm ET. Retirees and wanna-be retirees are welcome, in fact, welcome to anyone who is DESPERATELY SEEKING INCOME.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment